10 Facts about Private Equity

1. PRIVATE EQUITY IS NOT VENTURE CAPITAL.

Whilst VC is a subset of private equity, private equity typically refers to investments in well established, significant businesses.

Yes, venture capital is a FORM of private equity. But just because a thumb is a finger, does not mean all fingers are thumbs.

Think buy-outs, distressed asset special situations, growth equity.

2. PRIVATE EQUITY MANAGERS ARE NOT PASSIVE INVESTORS.

Unlike public equity, private equity managers take an active and strategic role in the companies they invest in. They are far more in control of the directions and destinies of the companies in which they invest.

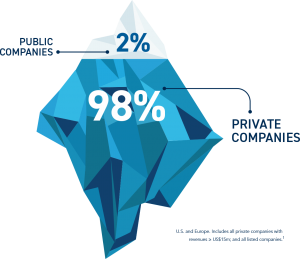

3. PUBLIC COMPANIES ARE JUST THE TIP OF THE ICEBERG. THE SIZE OF THE PRIVATE MARKET IS MASSIVE.

If you take number of privately held companies in the US and EU with over $15m in revenues, and add the number of all listed companies… Private Companies account for 98% of investable businesses1, but the access point to invest with the best of these private companies is next to impossible without a high-quality Private Equity manager.

4. PUBLIC MARKETS ARE SHRINKING.

The number of listed companies is declining, whilst allocation to private equity investments is growing.

The number of listed companies in the us has dropped to less than half of what it was in 1996, whilst the size of global private market investments has grown by about 700% since the year 2000.

5. PRIVATE EQUITY IS A REAL ASSET.

Private markets have outperformed public markets across 10 and 20 year time horizons, across multiple geographies such as US, UK, China.

6. PRIVATE EQUITY HAS ONLY REALLY BEEN AVAILABLE TO MAJOR INSTITUTIONAL INVESTORS.

Typical PE investment funds require minimum 5-10 million-dollar commitments.

This means that to build a diversified portfolio of PE investments one would likely need 10s of millions of dollars to allocate to PE within their portfolio.

7. TYPICAL PRIVATE EQUITY INVESTMENTS REQUIRE A 10-15 YEAR LOCK UP.

So not only do you need 10s of millions to invest in PE, you also need to be able to defer investment returns for 10-15 years.

8. MOST TOP QUARTILE PRIVATE EQUITY MANAGERS DO NOT NEED NEW INVESTORS.

The dispersion between top and bottom quartile private equity manager returns can be as large as up to 20%. (Whilst the difference in performance of listed equity managers is much smaller, likely around the 6% mark).

9. THE AVERAGE AUSTRALIAN INVESTOR IS UNDERWEIGHT PRIVATE EQUITY IN COMPARISON WITH THE LARGE INSTITUTIONAL INVESTORS.

Given it’s characteristics for higher returns and lower volatility, the average Australian investor is extremely underweight PE in their portfolios (compared to the future fund’s 14.1% allocation.)

10. THERE IS A PRODUCT ON THE AUSTRALIAN MARKET THAT IS COMPLETELY CHANGING THE BARRIERS OF ACCESS TO PRIVATE EQUITY.

PE1

A Listed Investment Trust for private equity is not dissimilar to a real estate trust that takes a typically large and illiquid asset and breaks it up into investable chunks on the stock exchange, PE1 represents an underlying portfolio of diversified global private market investments, managed by one of the largest and most established private market allocators in the world, Grosvenor Capital Management, in partnership with Australian fund management business Pengana Capital.