Listed private equity – capitalising the return premium

LISTED PRIVATE EQUITY; PRIVATE EQUITY REIMAGINED

In Part 3 of our 4-part series Listed Private Equity: Private Equity Reimagined, Consulting Economist Steven Milch shows that the superior long term returns of Private Equity can warrant a consistent and significant premium above a listed security’s Net Asset Value. We also discuss ‘persistence’ in private equity, whereby the top performing managers are able to consistently outperform over time.

CAPITALISING THE PRIVATE EQUITY PREMIUM

In Part 2 of our series, we discussed the attractiveness of Listed Private Equity as an asset class and the prospect that the prices LPE securities may be supported by investor demand. This raises the issue of the relationship between the market prices of LPE securities – which are subject to demand and supply influences – and the valuations or Net Asset Values (NAVs) of their underlying portfolios. Specifically, we explore whether LPE securities should trade at a premium or discount to NAV.

Jegadeesh et al[1] highlight the importance of expectations in the determination of market prices and, specifically, in the relationship between the market price of a listed PE security (which is determined in real time) and it’s NAV (which usually lags).

Using a present value methodology, the authors determine that a premium to NAV is consistent with investors expecting a return above the ‘cost of capital’ (which can also be thought of as an investor’s ‘required rate of return’). Conversely, a discount to NAV is consistent with investors expecting a return below the required rate.

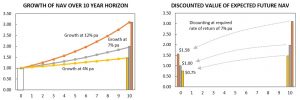

This is illustrated, using an illustrative example, in Chart 1.

CHART 1: THE ROLE OF EXPECTATIONS IN LISTED PRIVATE EQUITY

The example indicates that an investor who anticipates an investment rate return above their required rate of return may be prepared to pay more than a security’s NAV in order to ‘gain access to’ or ‘participate in’ the investment. In effect, the investor is capitalising the future return premium into the listed security’s valuation today.

This leads to the key conclusion that a LPE premium to NAV is rational and sustainable where investors anticipate an investment rate of return above their required rate of return. In other words, an expectation of consistently strong performance (based on factors such as fund manager resources, skill and track record) can validate a consistent premium to NAV.

A similar result has been found in relation to property securities. In a study of Australian REITs (real estate investment trusts), Erol et al[2] observe that the liquidity of REITs, relative to physical property, has contributed to the significant premiums above NAV evident in that sector since 2013.

Of course, financial markets and investors do not always operate rationally. At such times, securities may trade below NAV, despite factors such as return outlook and manager skill justifying a premium. Such instances, rather than invalidating the analysis above, may represent an opportunity to invest and accrue, over time, a return above that of the underlying PE portfolio.

Long term PE return expectations

We can take our analysis a step further (and add a degree of precision) by considering returns in the current environment. For this, we use global fund manager BlackRock’s[3] latest 10-year return expectations for shares and private equity (see Table 1).

| TABLE 1: LONG TERM INVESTMENT RETURN EXPECTATIONS (in AUD)

(% per annum, BlackRock Investment Intitute, August 2020) |

||||

| 5-year | 10-year | 15-year | 20-year | |

| Global Private Equity (buyout) | 11.7 | 12.4 | 13.0 | 13.3 |

| Global ex-Australia Large Cap Equities | 5.7 | 6.6 | 7.3 | 7.8 |

| Australia Large Cap Equities | 7.3 | 7.6 | 7.8 | 7.9 |

| US Large Cap Equities | 5.1 | 6.1 | 7.0 | 7.4 |

Using the same methodology as earlier, compounding an initial $1 investment at the 10-year annual PE return expectation of 12.4% yields a final value of $3.22. Discounting this at a required rate of return of 7.6% (here using the 10-year expected return for Australian Equities) results in a value today of $1.55. Hence, the capitalised value of the return premium in this (realistic) example is equivalent to a 55% premium above NAV today.

While individual investors will have a range of different expectations and time horizons, this provides some indication of the potential premium to NAV that a listed private equity security could trade at in the current environment – without appearing overvalued.

Manager expertise is paramount

So how realistic is it to expect consistently strong performance? Here, the literature finds evidence of PE performance ‘persistence’[4]; that is, the ability of top-performing managers to repeat strong performance over time.

Fleming[5], for example, states that “The returns to private equity investment are higher for more experienced managers”. Moreover, “returns exhibit persistence, with more experienced managers performing well over successive funds”. Fleming’s conclusion is attributed in part “to the specialist skills required to be successful in private equity”.

BCA Research[6] also discuss the proven ability of some firms to “repeat top-ranked performance time after time across multiple funds”, concluding that “manager selection is critical to building a successful private equity program”. BCA attribute this to certain managers having superior access to proprietary deal flows.

To conclude, not all LPE securities will always trade above NAV. However, where a proven PE manager with a performance track record is in place and the environment is supportive of long term performance, Listed Private Equity securities can rationally and sustainably trade at a premium above NAV.

In the final instalment of our series The Outlook for Private Equity Post-COVID we consider asset allocation developments, the impact of recent changes in the macroeconomic environment and longer term influences on the performance prospects for private equity.

REFERENCES

BCA Research, “Private Equity: Have We Reached The Top?“, 2018.

Blackrock Investment Institute, Capital Market Assumptions, August 2020, < https://www.blackrock.com/institutions/en-zz/insights/charts/capital-market-assumptions>.

Cambridge Associates, “The 15% Frontier, 2016, <

Erol, I. and Tyvimaa, T., “Explaining the premium to NAV in publicly traded Australian REITs, 2008-2018”, Journal of Property Investment & Finance, 2020, pp. 4-30.

Fleming, G., “Institutional Investment in Private Equity – Motivations, Strategies, and Performance“ in Cumming, D.J. ed, Private Equity: Fund Types, Risk, Return and Regulation, 2010, Chapter 2, pp. 9-29.

Gohil, R.K. and Vyas, V., Private Equity Performance: A Literature Review, 2016, The Journal of Private Equity, pp. 76-88.

Harris, R.S, Jenkinson, T. and Kaplan, S.N., “Private Equity Performance: What Do We Know?”, The Journal of Finance, 2014, pp.1851-1881.

Jegadeesh, N. Kraussl, R. and Pollet, J. M., “Risk and Expected Returns of Private Equity Investments: Evidence Based on Market Prices”, The Review of Financial Studies, 2015, pp. 3269-3302.ABOUT THE AUTHOR

Steven Milch

With a career as an economist and institutional investor spanning over 30 years Steven Milch (M Ec, B Comm Hons) has accumulated extensive financial market experience and a unique breadth of knowledge.

Steven currently holds postgraduate teaching positions with the University of New South Wales and Kaplan Business School. He manages assets in the not-for-profit sector and acts as Pengana Capital’s Consulting Economist.

Previously, Steven was Chief Economist and Head of Investments for the Suncorp Group. In this capacity, he led the Group’s Investment Research and Economics function and supervised the management of $21 billion of investment portfolios, focussing on asset allocation, manager selection and responsible investment initiatives.

Before joining Suncorp, Steven held the position of Chief Economist, St.George Bank. Steven has also worked at the Reserve Bank of Australia and has owned a successful investment advisory business. Steven is an investor in the Pengana Private Equity Trust (ARSN 630 923 643) (“PE1”).

IMPORTANT INFORMATION

Pengana Investment Management Limited (ABN 69 063 081 612, AFSL 219 462) (“Pengana”) is the issuer of units in PE1. A Product Disclosure Statement for PE1 (“PDS”) is available and can be obtained by contacting Pengana on (02) 8524 9900 or from www.pengana.com. A person who is considering investing in PE1 should obtain a copy of the PDS and should consider the PDS carefully and consult with their financial adviser to determine whether PE1 is appropriate for them before deciding whether to invest in, or to continue to hold, units in PE1. This report was prepared by Pengana and does not contain any investment recommendation or investment advice. None of Pengana, Grosvenor Capital Management, L.P., nor any of their related entities, directors, partners or officers guarantees the performance of, or the repayment of capital, or income invested in PE1. An investment in PE1 is subject to investment risk including a possible delay in repayment and loss of income and principal invested. Past performance is not a reliable indicator of future performance, the value of investments can go up and down.

[1] Jegadeesh, Kraussl and Pollet (2015).

[2] Erol and Tyvimaa (2020).

[3] BlackRock Investment Institute (2020).

[4] Gohil and Vyas (2016).

[5] Fleming (2010), p.24.

[6] BCA Research (2018), p.1 and p12.