Is now the time to buy REITs?

By Larry Schlesinger – Financial Review – original article

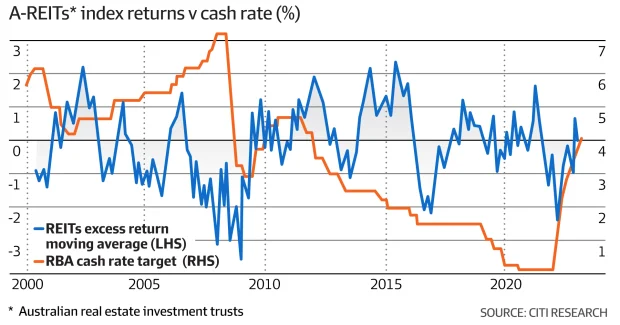

Australia’s listed real estate investment trusts– or A-REITs as they are commonly called – have endured a torrid time ever since the Reserve Bank started raising interest rates in May last year to curb inflation.

With higher interest rates have come higher yields on risk-free 10-year government bonds, making A-REITs – often regarded as bond proxies – less attractive to investors.

This is because the return premium between A-REIT yields (referred to as capitalisation rates in the sector) and bonds has shrunk sharply. Usually in the order of 200 basis points, the premium has been squeezed to less than 100 basis points for some commercial property classes.

As a result, A-REITs and REITs globally have been heavily sold down over the past 18 months, resulting in negative total returns of more than 20 per cent last year and almost 4 per cent over the first 10 months of what has been a volatile 2023.

“Why would I buy an office building on a 5 per cent cap rate when I get 4.5 per cent per risk-free?” explained Jefferies analyst Sholto Maconochie, succinctly.

But with an interest rate peak seemingly in sight – economists are tipping one more rate hike in February – and most of the big A-REITs reporting solid underlying operating performance, might it be time for investors to consider returning to the sector in 2024?

Some, like Pengana Capital Group fund manager Amy Pham, are already seeing opportunities in specific stocks and in sectors with favourable headwinds.

“We’ve recently taken a large position in [Westfield mall owner and operator] Scentre Group,” Pham says.

“The market is a bit cautious of weaker retail sentiment having an impact on retail malls owners, when in actual fact these malls have long leases locked in to over 300 retailers per centre. The majority of these retailers are national brands that have run their business through the hardest time during COVID and survived.

“On top of that these malls are very nearly full, with very favourable lease structures of [annual rental growth] of CPI plus 2.5 per cent, That’s really good rental growth in an asset that is very hard to replicate, and with high barrier of entry in fantastic locations,” she says.

Time to look forward

Pengana is also very keen on the alternative real estate sectors like childcare, healthcare, retirement living and data centres, which are not as cyclical as core assets such as office retail and industrial.

“If we have a rate rise or go into a recession, people still need childcare, healthcare and data,” she explains.

Pham also rates residential developer Stockland a “buy” given its very strong balance sheet and clear strategy, and because it does not have much exposure to the office market.

“The undersupply of housing especially affordable housing means Stockland is very well placed.”

More broadly, Pham says the headwinds hurting the A-REIT sector are largely in the rearview mirror, and it is now “time to look forward”.

The “key thing” to consider, she said, was whether an A-REIT is well positioned with a strong balance sheet to take advantage of any market dislocation opportunities and “set themselves up for next phase of the cycle”.

Looking at the potential for consolidation, Pham says takeover activity in the listed property sector is unlikely to be a feature of 2024 because the big fund managers that drive these deals are trading on low earnings multiples and takeover targets are highly geared.

“There may be a merger of equals, but not straight takeovers,” she says.

In assessing when is the right time for investors to look at A-REITs, and which stocks in particular are best positioned for a recovery, equity analysts at Citi Research examined how the sector had performance against the benchmark S&P/ASX 200 index over the last three interest rate cycles.

Citi’s key finding was that A-REIT outperformance starts zero to four months prior to the first RBA rate cut.

With a possible first-rate cut in the second half of 2024, Citi’s co-head of real estate research, Howard Penny, says the second quarter of next year might be the ideal moment to time a return to the REITs.

Beneficiaries of lower rates

As to which stock will be the biggest beneficiaries of eventual central bank rate cuts, Penny points to residential-focused stocks like Stockland and Mirvac, which are well positioned to benefit from strong consumer demand for housing.

He also likes defensive retail stocks like Vicinity Centres and Charter Hall Retail REIT, industrial powerhouse Goodman “which has historically performed very well” as well as fund managers like Charter Hall and GPT.

“Charter Hall and GPT are high beta value stocks meaning they fare worse in harder markets but do better in good markets. GPT is showing quite strong value at a 40 per cent discount to net tangible assets,” Penny says.

“In industrial, we still expect momentum to continue due to record low vacancy rates and demand outpacing supply. We’ve been one of the more optimistic broking houses on the retail sector, but favouring defensive, non-discretionary-focused portfolios.”

While the office sector might look cheap given steep discounts to NTA, Penny says the key fundamentals including supply outpacing demand and incentives and vacancy rates “grinding up” were still deteriorating. “We are cautious that office may be a value trap,” he says.

Taking a global perspective, J.T. Straub, head of real estate securities for North America at US real estate investment manager AEW, says many global REITs are offering “compelling valuations when compared with the private real estate market”.

Asked when would be a good time to consider returning to REITs, Straub says “now” as a general view, but very much dependent on market and sector.

“We feel that where REITs are priced at on a global basis is fair and compelling. Listed real estate offers very good valuations for growth going forward,” he says.